IADA predicts pre-owned aircraft sales uptick over next six months

IADA next six months 2023

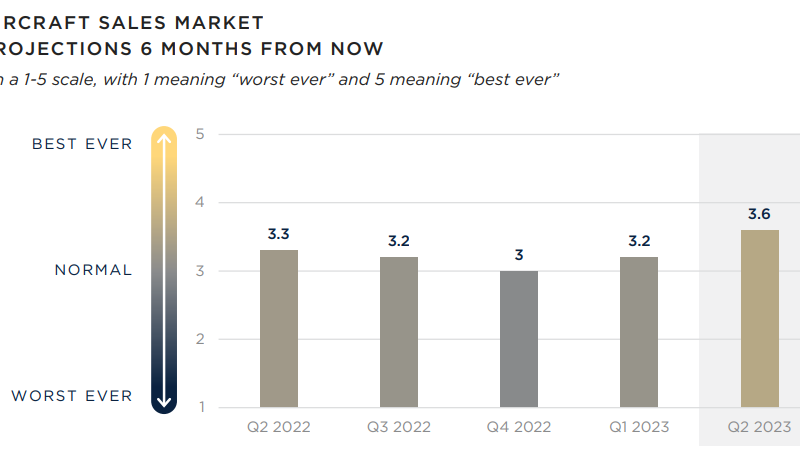

International Aircraft Dealers Association (IADA) members predict an uptick in pre-owned, private aircraft sales over the next six months, as noted in the organisation’s second quarter 2023 market report. It details an upswing in projections for the next six months compared with the preceding quarter and second quarter of 2022.

“IADA members, who lead the business aircraft resale marketplace, indicated a continuing normalization of the balance between buyers and sellers, with a nearly even split between which group is driving the market,” said Wayne Starling, executive director, IADA. “Their view of the market is cautiously optimistic, particularly given the vagaries of the global economy,” he added.

The perspectives and projections from IADA members for the IADA Market Report are supported by the monthly transaction activity reports submitted by IADA-accredited dealers through AircraftExchange, the online market listing portal. Results from the second quarter 2023 perception survey point toward a continuation of a modest slowdown in overall deals and somewhat softer pricing.

Overall deal flow in the second quarter of 2023 continued to be moderate. In addition to sales data from AircraftExchange listings, IADA’s market report includes data from all IADA-accredited dealer activities and transactions, reported in total.

In the first half of 2023, IADA dealers closed 542 deals, compared with 598 in the first half of 2022, which was an exceptional period in the resale industry. Aircraft resale prices for the next six months are projected to decrease slightly, across turboprops, light jets, midsize jets and large jets.

IADA members expect slight increases in aircraft supply for sale, also across all categories, with a stable willingness among dealers to inventory aircraft for sale. Demand is expected to be stable.

Based on IADA’s second quarter 2023 member survey and sales data provided by the network, respondents expect an ongoing shift toward a more balanced market throughout 2023. By recent historical measures, new aircraft manufacturer backlogs remain strong, but talent shortages and supply chain issues are constraining the ramp-up of production rates.

Business aviation, like other leading industries, continues to face challenges with geopolitical tensions, supply chain disruptions and the possibility of a US economic recession. Still, IADA brokers and dealers continue to see customer interest in owning or operating business aircraft.

IADA members have also reported that aircraft prices and valuations have come off their 2022 peaks, but they still see reasonably strong pricing for preferred makes and models with the right pedigree. Members are also seeing good activity in the long-range heavy jet sector, but have experienced longer times to close with a slight reduction in the number of transactions. There are concerns within the community over the collapse of a few of the charter/fractional providers, but the overall market outlook for preowned business aircraft continues to be broadly favorable for the foreseeable future. Read the report here.

IADA-accredited dealer members’ comments from monthly transaction reports

James Norris, Omni Aircraft Sales, Tulsa, Okla

“Overall buying interest is still present; however, buyers are now more concerned about the overall value they are getting from the purchase of an aircraft. Aircraft that are equipped well, have lower time, and great pedigrees are still getting a lot of love.”

Josh Mesinger, Mesinger Jet Sales, Boulder, Colorado

“More inventory coming to market daily, better more balanced buyer/seller due diligence and transaction terms and prices are going down, but at a healthy balanced market rate. We do not see a bubble bursting or any drastic price fall coming barring unforeseen major economic issues.”

Walt Wakefield, Jeteffect, Long Beach, California

“It’s hard to find pilots, parts, training slots and maintenance slots making transactions more difficult and taking longer.”

Mark Bloomer, Jet Transactions, Newport Beach, California

“Inventories are normalising, which promotes a delayed buyer response.”

Johnny Foster, OGARAJETS, Atlanta, Georgia

“For the buyer, more supply creates more opportunities and a greatly enhanced buyer experience. Value shoppers will find their deals in quarter three and we predict quarter four will be back to a feverish pace.”

Zipporah Marmor, IADA-Accredited Dealer ACASS, Montreal, Canada

“While the number of closings in the first half of 2023 has certainly been low, the level of activity has not. As such, I am optimistic that we will have a strong second half of the year.”

Frank Janik, Leading Edge Aviation Solutions, Parsippany, New Jersey

Here we are back to an even market where sellers nor buyers have the edge. The industry is less and less concerned about the correction that never came (so far). Prices have decreased but at a gradual rate and not even across all sectors (larger older cabins have declined more). Inventory has steadily increased, but we have seen very few if any distressed sellers or repossessions. Guidance to clients is that we are back in a normal market with prices on average trending down 7 %to 9% annually.”

Rohit Kapur, JetHQ, Kansas City, Missouri and Dubai, UAE

“Demand remains stable, though supply side will ease out, bringing out some corrections to the price.”